Finance for outdoor renovations refers to the diverse funding strategies available to homeowners for funding landscaping, decks, and garden structures. Common options in New Zealand include mortgage top-ups to leverage home equity, personal loans for rapid funding, and supplier-specific finance plans like Gem or Q Card for interest-free terms on materials and installation.

Assessing Your Financial Options for Outdoor Living

Transforming a backyard into a functional outdoor living space is a significant investment that requires careful financial planning. Whether you are installing a high-end louvre roof system, building a composite deck, or landscaping an entire section, securing the right finance for outdoor renovations is critical to the project’s success. In the current economic climate, understanding the liquidity of your assets and the cost of borrowing is the first step toward breaking ground.

New Zealand homeowners often prioritize “indoor-outdoor flow,” making these renovations not just lifestyle upgrades but strategic asset improvements. However, the scale of these projects often exceeds disposable cash reserves. This necessitates a deep dive into the lending market to find a solution that balances immediate cash flow needs with long-term interest costs.

Leveraging Equity: The Top-Up Mortgage

How does a mortgage top-up work for renovations?

A mortgage top-up involves increasing your existing home loan limit to access the equity you have built up in your property. This is widely considered the most cost-effective method for financing substantial outdoor renovations.

Because the loan is secured against your property, banks can offer interest rates significantly lower than personal loans or credit cards. For example, if you have owned your home for several years, market appreciation and principal repayments likely mean your Loan-to-Value Ratio (LVR) has improved, giving you borrowing power.

The Application Process

To secure a top-up, your bank will assess your current income, expenses, and the estimated value of your property. For outdoor renovations involving permanent structures (like pergolas or retaining walls), the bank may require:

- Quotes and Estimates: Fixed-price quotes from contractors to prove the funds are for property improvement.

- Registered Valuation: An updated valuation to confirm your equity position.

- Council Consents: Proof that the planned work complies with local zoning and building standards.

Pros and Cons of Top-Ups

Pros:

- Lowest possible interest rates (residential home loan rates).

- Flexible repayment terms spread over the life of the mortgage (up to 30 years).

- Consolidated debt within a single banking relationship.

Cons:

- Spreading a small renovation cost over 25-30 years can result in paying a massive amount of interest in the long run unless aggressive repayments are made.

- Requires a formal application process and potential valuation fees.

- Increases the total debt secured against your home.

Supplier Finance Plans: Gem Visa & Q Card

Are supplier finance cards good for renovations?

Supplier finance plans, such as Gem Visa, Q Card, and Purple Visa, are excellent tools for short-term cash flow management, provided they are managed with strict discipline. These options are frequently offered by outdoor furniture retailers, landscaping supply stores, and shade structure specialists.

These financial products typically offer “interest-free” or “deferred payment” periods ranging from 6 to 48 months. This can be incredibly advantageous if you have the cash flow to service the debt within the interest-free window but lack the lump sum upfront.

Understanding the Fine Print

The danger of supplier finance lies in the reversion rate. Once the interest-free period expires, the interest rate often jumps to a high percentage (often between 25% and 28% p.a.).

Strategy for Success:

- Calculate the Weekly Payment: Divide the total cost of the renovation by the number of interest-free weeks.

- Set Up Automatic Payments: Ensure this calculated amount is paid automatically to clear the balance exactly before the promotion ends.

- Factor in Establishment Fees: Most cards charge an annual fee and an establishment fee, which adds to the total cost of credit.

This method is ideal for medium-sized purchases, such as a spa pool, outdoor kitchen cabinetry, or high-end paving stones, where the cost is between $2,000 and $15,000.

Personal Loans and Construction Finance

When you do not have sufficient equity for a mortgage top-up, or if you wish to avoid extending your home loan term, a personal loan is the middle-ground option. Personal loans for home improvements are unsecured (usually) and processed much faster than mortgages.

Speed vs. Cost

The primary benefit of a personal loan is speed. Approval can often be obtained within 24 to 48 hours. This is crucial if you need to secure a contractor’s slot or purchase materials during a sale. However, interest rates for personal loans are higher than mortgages, typically ranging from 8% to 16% depending on your credit score.

Green Loans

Some New Zealand banks now offer “Green Loans” or “Warm Up” loans at very low interest rates (sometimes 0% or 1%) for energy-efficient upgrades. While usually targeted at insulation and heating, some outdoor projects that involve solar lighting, water retention systems, or sustainable materials may qualify. It is worth investigating if your outdoor renovation has an eco-friendly angle.

Strategic Budgeting for Staged Builds

How can I renovate without a loan?

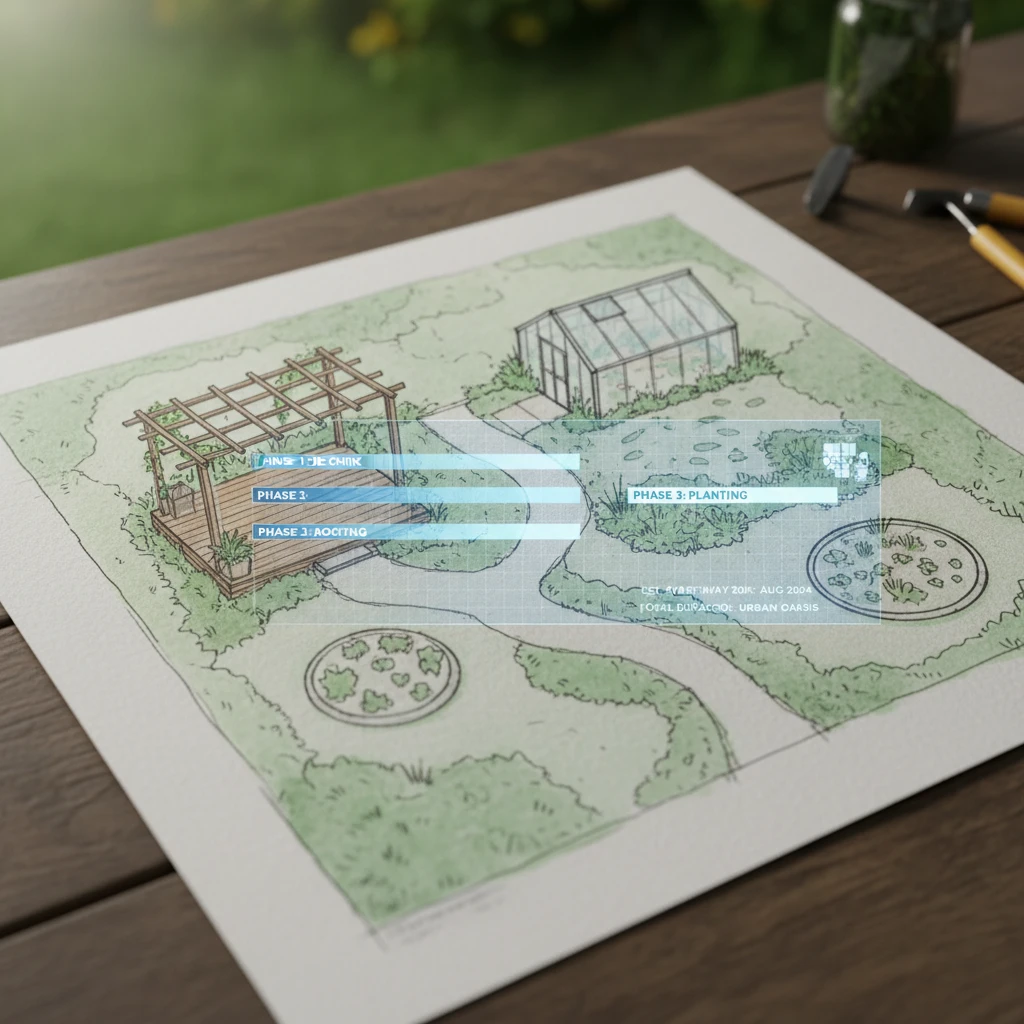

If taking on debt is not an option, the most prudent financial strategy is the “Staged Build” approach. This involves breaking your outdoor renovation master plan into financially manageable phases.

Phase 1: Hardscaping and Infrastructure

Allocate your initial budget to the “bones” of the project. This includes earthworks, retaining walls, concrete pads, and decking. These elements are disruptive to install, so getting them done first is essential. It is difficult to add drainage under a deck once it is built.

Phase 2: Overhead Structure

Once the savings replenish, install the pergola or louvre roof. Many modern systems are modular, allowing you to install the frame and roof now, and add drop-down screens or glass sliding doors later.

Phase 3: Softscaping and Finishing

The final stage involves planting, lighting, and furniture. These items are lower cost and can be purchased gradually. This approach requires patience but ensures you remain debt-free throughout the process.

ROI: Adding Value to Property Appraisal

When securing finance for outdoor renovations, it is vital to view the expenditure as an investment rather than a cost. In the New Zealand property market, outdoor living spaces are premium selling points.

The Appraisal Boost

Real estate agents frequently cite “indoor-outdoor flow” as a top requirement for buyers. A well-executed outdoor area effectively increases the livable square footage of the home. For example, a 20-square-meter deck with a high-quality roof system can function as a second living room.

High ROI Outdoor Projects:

- Decks and Patios: typically recover 70-80% of their cost in added property value.

- Outdoor Kitchens: appeal to the luxury market and differentiate the property.

- Fencing and Privacy: essential for families with pets and children, adding immediate marketability.

When applying for a top-up mortgage, presenting the renovation as a value-add project can help in discussions with bank lending managers, as it reassures them that the security (your house) is increasing in value.

Navigating Hidden Costs and Contingencies

Regardless of the finance option chosen, borrowing the exact amount of the quote is a rookie error. Outdoor renovations are notorious for hidden costs.

The Contingency Fund

Financial experts recommend adding a 15% to 20% contingency buffer to your loan application. Common surprises include:

- Excavation Issues: Hitting rock or discovering poor soil quality requiring deeper piles.

- Drainage Requirements: Council requiring upgraded stormwater management due to increased impermeable surfaces.

- Material Price Fluctuation: Timber and steel prices can fluctuate between the quote date and the purchase date.

If you borrow via a top-up mortgage, you can often leave the contingency portion in a revolving credit facility (offset account). If you don’t use it, you don’t pay interest on it, but it is there if needed.

People Also Ask

Can I use my KiwiSaver for outdoor renovations?

Generally, no. KiwiSaver is designed for retirement or your first home purchase. Under current legislation, you cannot withdraw KiwiSaver funds for renovations, repairs, or home improvements unless you can prove significant financial hardship, which is a rigorous process not intended for upgrades.

Is the interest on renovation loans tax-deductible?

For a standard owner-occupied home in New Zealand, interest on renovation loans is not tax-deductible. However, if the renovation is for a rental property or a business premise (e.g., a home office extension), you may be able to claim interest expenses. Always consult a tax accountant for specific advice.

How much does a typical outdoor renovation cost in NZ?

Costs vary wildly based on scope. A basic timber deck might cost $400-$600 per square meter. A high-end automated louvre roof system can range from $15,000 to $40,000+. A full landscape transformation including retaining, planting, and hardscaping often sits between $30,000 and $80,000.

What is the difference between a fixed and floating rate for renovations?

A fixed rate locks in your interest percentage for a set time (e.g., 2 years), providing certainty for budgeting. A floating rate moves with the market but allows you to make lump sum repayments without penalty. Many renovators use a floating rate for the renovation portion of their mortgage to pay it off aggressively.

Do I need council consent to get finance?

Banks often require proof of council consent for structural additions before releasing funds for a mortgage top-up. This ensures the asset they are lending against is legally compliant. Personal loans and credit cards generally do not require this documentation.

Does landscaping increase property value more than interior renovation?

Not necessarily more, but often with a better cost-to-value ratio. While kitchens and bathrooms sell houses, street appeal and outdoor living are what get buyers through the door. In New Zealand’s climate, a functional outdoor area is often expected by buyers in the mid-to-high price bracket.